Posted by Linda Rowings Premium tax credits are only available to individuals who obtain health coverage through a Marketplace. A dispute has arisen as to whether the IRS has the ability to interpret PPACA to allow the subsidy to individuals who obtain coverage through any Marketplace, or whether the language of PPACA limits eligibility to … Continued

(NewsUSA) Americans catch approximately 1 billion colds each year, and the Centers for Disease Control and Prevention estimates that as many as 20 percent of people in the U.S. will get the flu this cold and flu season. A majority of people (seven in 10) will use over-the-counter (OTC) medicines to treat their symptoms, and … Continued

Data in the 2014 UBA Health Plan Survey is based on responses from 9,950 employers sponsoring 16,967 health plans nationwide. Results are applicable to the small to midsize market that makes up a majority of American businesses, as well as to larger employers, providing benchmarking data on a more detailed level than any other survey. To help employers benchmark their health plan costs by organization size, the chart below shows average costs in descending order.

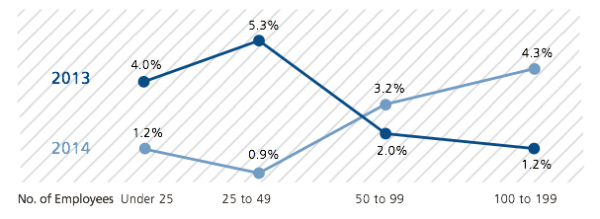

Looking at the smallest employer groups, the 2014 findings show an interesting flip in rate increase patterns. Contrast this with last year’s findings, which showed the following increases over 2012 among the same groups.

Historically, employers with 1 to 49 employees felt the brunt of increases, which ranged from 4% to 5% or more. However, in this year’s survey results, these groups saw more modest increases of approximately 1%. Conversely, employers with 50 to 199 employees have historically had more modest increases of 1% to 2%, while this year they saw increases of approximately 3% to 4%.

The ability for small groups to “renew as is” (by grandmothering or by delaying renewals) is having a huge impact on keeping their rates level, at least at this point. Many small groups had the choice of moving to a PPACA-compliant plan or staying with the plans they had (thanks to grandmothering in some states and other delay tactics). Healthy groups tended to stay with the plans they had, which often was the most cost-effective approach. As these groups move to PPACA-compliant plans and become subject to community rating, they will likely see significant cost increases. But this year, they had a reprieve.

Since 2005, United Benefit Advisors® (UBA) has surveyed thousands of employers across the nation regarding their health plan offerings, their ongoing plan decisions in the face of significant legislative and marketplace changes, and the impact of these changes on their employees and businesses. The UBA survey represents the nation’s largest health plan benchmarking survey and the most comprehensive source of reliable benchmarking data.

As always, the survey revealed several noteworthy trends and developments that bear scrutiny and the ongoing attention of employers interested in making the most informed health care plan decisions possible. For example, among the most striking trends revealed by the survey, employers have overwhelmingly opted for early renewals of their plans—a delay tactic that helped them avoid costly Patient Protection and Affordable Care Act (PPACA)-compliant plans and manage costs. Another cost management tactic employers are using is to increase out-of-pocket costs for employees, with a “new normal” emerging for these higher cost thresholds.

Employers typically continue to offer one preferred provider organization (PPO) health plan option to employees, while also still widely offering family coverage. In addition, wellness program adoption seems to be in a holding pattern, as pending litigation and regulatory changes swirl on these offerings. Among employers providing wellness programs, health risk assessments and incentives are increasingly common offerings.

Plans in the Northeast U.S. continue to be the richest—and most expensive—and are at risk of being subject to the looming Cadillac tax. Government employees have the most generous plans with the highest costs—and they pay the least toward their overall coverage costs. Conversely, construction industry employees cost the least to cover but those employees pay the most toward costs.

Regarding cost increases, the smallest employers (0 to 49 employees) saw the lowest increases, a surprising break for them due to an unusual option they had over larger employers to remain with non-PPACA-compliant plans. In short, this was a reprieve for a group that usually faces the highest increases. Self-funding of plans, particularly among small employers, has not yet surged, but is still anticipated to do so as employers run out of other avoidance strategies.

The prevalence of consumer-driven health plans (CDHPs) continues to grow, as does employee enrollment in these plans, despite lower contributions to health savings accounts (HSAs) (which are often tied to CDHPs to entice participation). And, finally, prescription drug plans are increasingly offering four or more tiers, along with ever-increasing copays—a trend that might fall off as they must all eventually tie to out-of-pocket maximums under PPACA.

Question: What are the Employee Retirement Income Security Act (ERISA) rules about nondiscrimination in benefits plan designs to assist with creating benefit class carve-outs? Answer: Under the Health Insurance Portability and Accountability Act (HIPAA, which is governed by ERISA) and I.R.C. § 125 plan rules, employers are allowed to offer different contribution levels or benefit … Continued

Question: Are we required to have employees complete wellness reward screenings which impact health care premiums, prior to the new plan year beginning? Answer: While some employers do take this approach, it may be possible for employers to apply premium reductions for those who complete the required screenings mid-year. The challenge relates to compliance with … Continued

By K. Michael Ward, MPH, SPHR, GPHR, Employee Benefits Advisor The Wilson Agency A UBA Partner Firm

As a business professional who is trying to classify a worker, it is important to remain compliant with the IRS regulations that determine whether an individual providing services to your organization should be classified as an independent contractor or an employee.

Furthermore, the “employer mandate” section of the Patient Protection and Affordable Care Act (PPACA) requires companies with 50 or more employees to either provide adequate and affordable coverage to their workers or pay tax penalties. United Benefit Advisors (UBA) has developed a guide to help employers determine how many employees they have for several purposes under PPACA. Those who think they are exempt need to make sure they are counting employees correctly so they’re not surprised with penalties.

The guide provides the definitions of full-time employees, how to count part-time employees on a pro-rata basis, how to treat seasonal employees, who the law considers an “employee,” counting hours correctly, determining average hours worked, penalties that result if a “large employer” doesn’t offer coverage, applying the requirement to offer coverage, paying the penalty, and eligibility for the Small Business Health Options Program (SHOP).

Your UBA Partner Firm can help you find the compliance solutions specific to the issues your company is facing. Visit the UBA website to learn more.

Why does it matter?

Not correctly classifying an individual as an employee can lead to an employer being required to pay taxes, such as unemployment tax, that would have been required of the employer if the individual had been correctly classified. The organization may also be held liable for overtime pay, resulting in a costly expense for the organization. In certain situations, the issue can escalate leading to civil lawsuits against the employer.

How do I know how to classify individuals?

Generally, an individual is an independent contractor if the employer controls only the final result of the work and not when, where and how it will be done. Therefore, employers cannot demand that independent contractors work a “9-5” schedule in their office. If the person is an independent contractor, they are free to perform the work on a beach at 4 a.m., as long as they produce the services for which they were hired.

An individual may also be classified as an employee if the company provides the majority of the equipment used to perform the services. Independent contractors will generally work with their own equipment and are unlikely to be reimbursed for any equipment purchases required to perform the job.

Some others factors to take into consideration are the time period of hire and whether the individual provides services that are integral to the business. If an individual has been hired on an indefinite basis, versus for a specific project or time period, and/or provides key services, then the employee may be classified as an employee.

There are a variety of other nuances that can determine whether an individual is an independent contractor or an employee. Therefore, it is advised that you speak with a professional before taking action that could have an adverse effect on your business.

On November 4, 2014, the Departments of Health and Human Services and the Treasury released Notice 2014-69 regarding employer-sponsored health plans and the Affordable Care Act (ACA) definition of minimum value coverage. The Notice clarifies that plans that do not “substantially cover in-patient hospitalization or physician services” — often called “skinny” or “bare bones” plans … Continued

By: Peter Freska, MPH, CEBS, Benefits Advisor The LBL Group A UBA Partner Firm

We field many call to review, speak, and comment on a variety of topics. Of course, these generally pertain to health care. In preparing for a coming presentation, I came across a recent article in Becker’s Hospital Review titled “100 Healthcare Statistics to Know”. While there are many topics that comprise health care, the article breaks them down into 10 categories: Hospital and Physician Facts, Hospital and Health System Compensation, Health Coverage, Medicaid, Medicare, Hospital Construction, Accountable Care Organizations, Health IT, Patient Care and Quality, and Miscellaneous Health Care Statistics. While all these topics are important, of particular interest is the section on health coverage:

Roughly 10.3 million adults in America gained health coverage between January 2012 and June 2014, according to a study published in The New England Journal of Medicine.

In 2014, the number of uninsured Americans dropped by 3.8 million from January to March, which brought the average percentage of people without health insurance to 13.1%, according to a survey by the Centers for Disease Control and Prevention’s National Center for Health Statistics.

On average, health care cost nearly $9,000 per person in 2012, according to the Bureau of Labor Statistics.

On average, health care for a typical family of four covered by an employer-sponsored preferred provider organization plan currently costs roughly $23,215. That cost is nearly twice what it was a decade ago, but the year-over-year increase of 5.4% between 2013 and 2014 is the lowest growth rate recorded by the Milliman Medical Index since it was first calculated in 2002.

National health care spending is projected by the Centers for Medicare & Medicaid Services to increase 4.7% from 2013 to 2015.

In reviewing these statistics against the United Benefit Advisors (UBA) 2014 Health Plan Survey* (which is the nation’s largest and most comprehensive benchmarking survey of plan design and cost), I came up with some interesting comparisons. First, it is important to note that the UBA 2014 Health Plan Survey database contains the validated responses of 16,467 health plans, sponsored by 9,950 employers, who cumulatively employ nearly one million employees and provide coverage for more than four million total lives. Individually validated responses from employers in more than 3,000 communities in all 50 states and the District of Columbia complete the database.

To compare a few statistics, the outlined health care cost was “nearly $9,000 per person in 2012.” The 2014 UBA Health Plan Survey indicates an average plan cost of $9,504 with an average employee cost of $3,228 and an average employer cost per employee of $6,276.

Premium increases are now an average of 5.6% for all plans – up from 5.5% in 2013.

Related to the premium increases are plans that have been able to hold out on making changes – “grandfathered,” and now so called “grandmothered” plans.

Employers delaying their health plan renewal dates until December 1 increased 322% from 2013 to 2014. Approximately 32% of employers postponed their renewal date, 94% of which were small businesses in the fewer than 100 employee market. In the fewer than 50 employee group size, there was more than five times the number of renewals for December 1, 2013, over 2012.

Driving large employers (1,000+ employees), is their ability to more easily self-fund.

10.6% of all plans are self-funded, with more than three-fourths (80.0%) of all large employer plans self-funded.

These measures continue to indicate that self-funding is moving down market, as smaller employers are working to avoid premium increase and the Health Insurer Transitional Tax (HIT Tax). A move to self-funding from a fully insured plan will allow an organization to recognize a 2% to 7% (nationally) HIT tax.

Knowing the numbers, and having the ability to benchmark employer plans, is paramount – especially with so many changes driven by health care reform. Current, validated data allows employer plans to make the best informed decisions to benefit the organization as well as the employees and families to which they provide benefits.

* Data in the 2014 UBA Health Plan Survey is based on responses from 9,950 employers sponsoring 16,967 health plans nationwide. The survey’s focus is intended to provide a current snapshot of the nation’s employers rather than covered employees. Results are applicable to the small to midsize market that makes up a majority of American businesses, as well as to larger employers, providing benchmarking data on a more detailed level than any other survey.

CLICK HERE to pre-order a copy of the 2014 UBA Health Plan Survey Executive Summary or CLICK HERE to request a customized benchmarking report.

“In the rapidly changing implementation of PPACA, it is critical for businesses to know their benchmark on medical plans,” says UBA CEO Les McPhearson. “This is not only for their industry, but in their state, region and nationally as well. I’d encourage employers to look at the UBA Health Plan Survey in a way that is most relevant to their business.”

The 2014 UBA Health Plan Survey offers more than national data and UBA recommends that employers benchmark with local data, which is more effective when adjusting plan design, negotiating rates, and communicating value to employees.

By Leigh A. Zaykoski The 10-panel drug screen test is a drug test method that screens for 10 drugs. This type of test can detect several illegal drugs as well as high levels of prescription drugs that have the potential for abuse. The test procedure is relatively simple and provides results in three to eight … Continued